The biggest side-story to come out of the Manchester City judgment is how “Premier League clubs with high levels of borrowing are now in danger of breaching Profitability and Sustainability Rules.”

Arsenal have been made the poster boy of the statement, with many journalists going onto point out that we “have borrowed more than £200m made up entirely of shareholder loans.”

The insinuation is then that we have found a loophole within the rules to find our rise back to title challengers, and that we are hypocrites for our stance against Manchester City. But this is not true, and to tell the story, we need to go back to where it begun.

The stadium build

As with every club that builds a new stadium we required bank loans to do so.

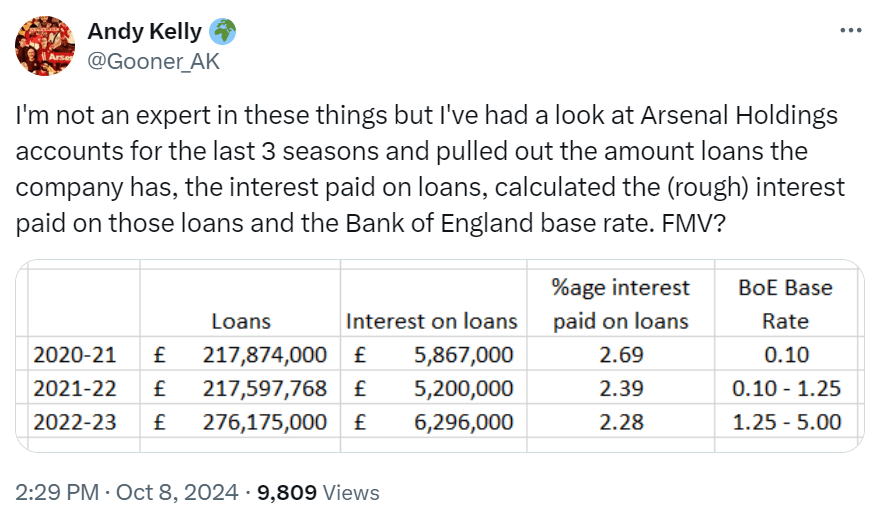

In 2007, we refinanced these into a new series of loans and bonds, spreading the debt over the next 25ish years. At the time the Bank of England base rate was 5%, and our average bond interest rate was 5.14%.

2020 refinancing

In the late 00s and early 20s, borrowing was dirt cheap. The Bank of Interest base rate went to as low as 0.1%. And then Covid hit which had many experts predicting interest would sharply rise (and it did). KSE then took the chance to refinance our debt.

KSE took a loan out themselves, and in turn loaned Arsenal the money to pay off the existing loan from the stadium including early repayment charges. The net gain was that whilst Arsenal would owe more money due to having to pay the charges, our total to be repaid, including interest, would drop.

Refinancing is a common practise in both business and life. Why pay more for interest than you have to? It is like changing mortgage provider to get on a lower rate.

Lower rates were available on the market that we were paying, so KSE decided to reduce what the club would pay, even though it meant increasing out total debt.

But is it Fair Market Value

A tagline to come out of the Manchester City case is “Fair Market Value (FMV)”. And I agree with City that shareholder loans should also be at FMV.

No more zero percent loans like what both Manchester City and Chelsea have benefited from in the past. Shareholder loans should be provided at a FMV rate. And there is zero evidence that Arsenal’s loans are not at FMV:

To establish what FMV is, we only need to look up the Seven Sisters Road.

Tottenham’s stadium loan is at 2.6% interest. Taking into account our Loan to Value (to use a mortgage term), will be a lot less than Tottenham, we would expect the interest rate offered to also be slightly less. And it is. So if the above is true and that we are paying around 2.4% interest, than KSE are clearly providing us with a shareholder loan at FMV.

Injecting cash to compete

A false narrative being written by opposing fans is how we have borrowed £200M of our owners so we can compete with the big boys. the irony of this is us Arsenal fans have complained for nearly two decades about the lack of investment from KSE into the club.

And this loan is not an investment into Arsenal to allows us to compete. It is a refinancing of existing date which goes back to the stadium build.

The Kroenke’s did not go out in 2020 and give us over £200m to buy players and spend on wages. The loan was to pay off the existing debt, held at 2007 interest rates, and then add new debt to the club at lower interest rates.

Debt from infrastructure costs excluded from PSR

From Day One of PSR, debt accrued from infrastructure improvements were always excluded from PSR.

Building or maintaining a football stadium comes under the ‘in the general interests of football‘ clause, which also includes the costs of running the women’s team and the academy.

It is this clause which has allowed Manchester City to massively improve the Eastlands without impacting on PSR. That has allowed Tottenham to build a new stadium. That allowed Liverpool to expand their stadium. And that will eventually allow both Newcastle United and Chelsea to build new stadiums.

If debt incurred by building or maintaining a stadium was accountable under PSR, then no club would rebuild a new stadium. Or develop their current one. Nor would they invest as much money into either women’s football (a loss-maker for every English club) or the academy. All of these would be at the detriment of English football.

So regardless of whether or not the shareholder loan from KSE is at FMV, as long as we can prove that the loan was for infrastructure then it does not nee be submitted as part of our PSR monitoring. And we can prove it was for the stadium as we can show the receipts of us receiving a loan to almost the same value as the bonds we paid off that were raised in 2007.

Zero PSR concerns

Those that are creating a narrative that Arsenal have somehow used a loophole to circumnavigate PSR, or have future PSR concerns are doing so with a lack of knowledge.

They have neither taken into account that the loan from KSE is at FMV, and that the loan relates to infrastructure improvements.

Reading social media, you would think Arsenal had been given a £200m interest free loan from KSE to buy players in 2020. But we did not. The two clubs to have been given sizable interest free shareholders loan this century are Manchester City and Chelsea.

And my final thought is that if new rules come in banning shareholder loans altogether, then they will not be bought in retrospectively. Any club currently with a shareholder loan will be able to continue operating with it without paying it off.

And the worse case scenario is we merely take out a bank loan (still at lower than the 2007 rates), pay back the KSE shareholder loan, and return to monthly payments to our new creditor. Basically using Peter to pay Paul.

For opposing fans reading this, I hope you now feel educated. Although I imagine all of you will ignore the facts and continue to with the narrative that Arsenal are in the wrong. IF you maintain that standpoint, then good luck in life. You will need it.

Keenos